It's three weeks into January 2021. How are you doing so far with your financial to-do list?

If you've implemented the financial checklist we've shared with you, you should be at the goal-setting stage or, at least, working out the details.

Well, let us help you move things along.

The objective is to set SMART financial goals. Do you remember? It's the surest way to ensure you achieve what you set out to do money-wise since you'll have a map that will serve as your guide.

Setting goals, however, is easier when you understand the premise behind the idea and the entire process.

What does it mean to set SMART goals?

Simply put, it's creating a financial goal that is concrete and specific, complete with a realistic strategy on how to achieve it.

Say you want to pay off all $5,000 of your credit card debt by the end of 2021. This means you’ll have to allocate approximately $420 every month to make this happen and not use the card for any purchases in the next 12 months. That’s a clearer plan than simply saying you want to pay your debts.

A smart financial goal turns a vague plan into something achievable within a specific timeframe because you have a clear idea on the HOWs based on your actual personal finance.

It also transforms a lofty goal such as investing into something feasible because you'll know exactly what elements are necessary to make this happen.

How do you set and achieve SMART financial goals?

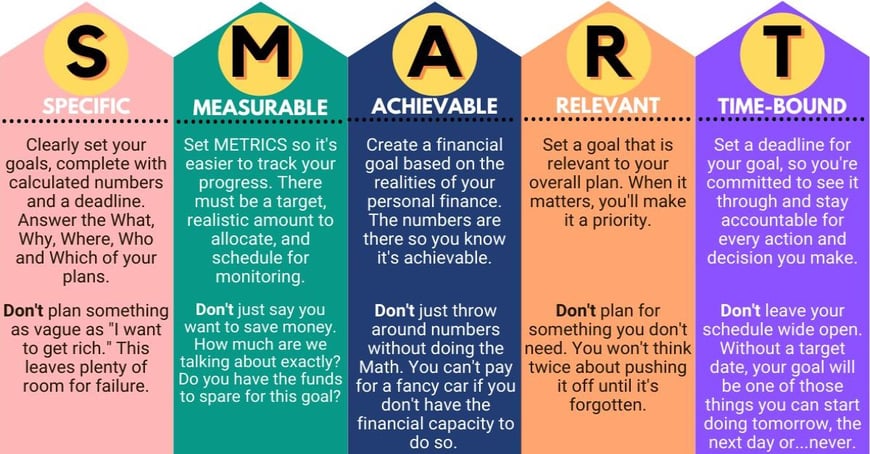

SMART stands for Specific, Measurable, Achievable, Relevant, and Time-bound. Understandable enough, right?

You know what each word means. You just need to understand how each one plays a role in your personal finance.

You’ve had an overview of SMART goal-setting in our previous blog, so we’re getting deep into it this time.

Specific

A specific goal answers the questions What, Why, Where, Who and Which.

Say you plan to start investing in currencies or stocks this year.

What exactly do you want to accomplish? Do you want to have more income, to be debt-free or to have a better financial future?

Why do you want to do it? Is it because you want more from life or that the goal aligns with the transformations you want to make this year?

Where will you source the funds for this particular goal? Are you going to funnel a small percentage of your savings account into investing and then augment it with extra funds from your income?

Who do you need to work with to achieve your goal? If you're new to investing, working with mentors or joining free webinars is a good idea.

Which challenges or constraints do you foresee? The earlier you know, the sooner you can set up solutions and contingency plans.

By listing down all the answers, you’re going to see what you need and what you have to face to make your plan attainable.

Measurable

It's important that you can measure your progress, so you'll know if you're on track to achieving your goal or far from it. In the case of personal finance, there are three metrics you must set:

- Target

- Financial capacity

- Checks and balances

Say, for example, you want to start investing.

How much financial growth do you want to see from your investing efforts? Your target can be $1,000, $5,000 or $10,000.

How much money do you need to set aside for this endeavour? Calculate based on what’s left after all expenses are paid, maybe after you’ve funnelled 10% to your savings account, and left a small amount for unexpected spending. Adjust your target according to the result.

How often are you going to check on your progress? Check your equity at least a month or every quarter to see if there’s growth or that the funds you invested are intact. If you actively trade, you should see your progress regularly. To see the numbers go up will motivate you further.

It’s important to be realistic and honest with your financial situation. You’re more likely to fail if you set a goal that’s impossible to achieve. This brings us to the next point.

Achievable

What's the point of setting a goal that is impossible to reach? You're basically planning to fail if this is the case.

If you want to invest this year, you should know that you have the capacity to do so. If you're deep in debt, you should make it your goal to pay it off first rather than invest.

While you may think that investing can double your money and help you achieve debt freedom quickly, it's impractical to do so when the interests pile up.

Setting an achievable goal means being practical and honest with your financial situation. This is where you need to research your personal finance. Find out how you can follow through with your goal without robbing you of occasional indulgences.

Relevant

The goals you set must be relevant to your life or situation right now. Otherwise, it will become just another plan you can afford to push back.

For example, you plan to start investing this year because it's relevant to your overall plan of building your wealth.

You want to increase your contribution to your retirement fund because you want to retire early.

The more relevant your financial goals are, the easier it will be to make sacrifices. Because the goals you set may require you to trim back on your spending or give up an indulgence. If this is something that is hard to do, your plans could fall through.

Time-bound

You must set a specific timeframe to achieve your goals. It doesn’t matter if you set a short-term or long-term timeline as long as you do. Without it, you could end up procrastinating and moving the goal post further than originally planned.

A deadline will also keep you accountable and make your plans that much more important. When was the last time you submitted a project beyond the deadline? You don't.

Time-based goals also create a sense of urgency and motivate you to work on them even if crises were to arise along the way.

Just so everything’s clear, here’s a summary of what to DO and NOT DO when setting SMART goals:

One other important thing...

You must develop a positive money mindset. Your relationship with money will dictate how you’ll perform with your financial goal. If you only see it as a means to spend on things you want, you’d fail to see how you can leverage it to achieve financial freedom and build wealth that will set you up for life.

So take a long hard look at how you value money. You know you’re ready to set your goals in motion if you see money as a means to achieve your objectives.

Here’s an exercise on SMART goal-setting

For illustration purposes, let's say your goal is to establish additional or multiple streams of income. You want your finances to be stable enough to weather any disruption, such as a recession, job loss or a pandemic, that may come your way.

Learn How to Prep Yourself Financially in Times of Crisis and avoid the same situation in the future.

How do you create a specific goal for this?

Remember the five W’s you need to answer to arrive at a specific plan.

- What: I want to start investing.

- Why: To earn an additional income and ensure financial stability.

- Where: Invest the extra money left after all expenses have been paid.

- Who: Learn from gurus/mentors and watch webinars or tutorials.

- Which: Unexpected expenses might come up. You could get sick and pay out of pocket to see a doctor.

By answering these questions, your goals take on a concrete form rather than just a vague idea. You’ll see the purpose of what you’re doing and what challenges you must prepare to face.

How do you measure your progress?

How much income growth do you want to achieve? $10,000

How much money can you set aside every month? $900

How will you measure your progress? You'll check in every three months. Your base capital should be $2,700 in the first month and you should see at least 3% growth in your equity, depending on your investment activities.

Reinvest what you earn and you might be able to achieve your goal earlier than expected.

Do you think your plan is achievable?

Based on the metrics you set, it's clear that your goal is attainable. You do have the funds to spare. If you simply want to save money, you can easily save $10,000 in a year if you diligently put $900 towards your savings account every month.

Since you're investing in currencies or stocks, you could hit your goal earlier if all your investment decisions have positive returns.

Combine this with a strong will to resist the urge to spend the extra money elsewhere or simply rely on your investment profit to cover the cost, and your goal is more than attainable.

Here’s why you should invest in Forex during a recession or pandemic.

Is your goal relevant to your life or overall plan?

If your desire to have multiple income streams stems from the fact that your finances took a beating during the pandemic, then it's definitely relevant. The same is true if you plan to make wiser financial decisions this year.

You realised that relying solely on your income and what little savings you have is not enough. It only makes sense that you should start adding another layer of security to your finances now that you have the resources and capability to do so.

How long before you achieve your goal?

You want to hit your goal in 12 months and your calculation shows you can definitely make this happen. The deadline will keep you accountable and help you stay committed to your objective.

As you approach the 12-month mark and your investments show positive returns, you will see that nothing is impossible with a sound plan.

Now that you have all the details, your simple goal of having additional income becomes a SMART one--earn an additional $10,000 in 12 months by investing $900 every month in currencies or stocks and reinvest the profit.

Just looking at that statement makes your plans real and highly attainable.

Ready to grow your wealth and generate additional income from the world's largest financial market? No better place to start than right here with us! Begin trading with Fullerton Markets today by opening an account:

You might be interested in: How to Trade Forex Even With a Full-time Job and Earn on the Side