The most notable fact about the trading action this week is how quiet it has been compared to the previous two weeks. Well, it is not that bad. The CBOE Volatility Index, which began on March 19 and went to 30 in the middle of the month, is back to 19.

Activity in the S&P Bank ETF, where the normal average volume was one to two million shares daily before the banking crisis, saw multiple days with a volume of over 11 million shares two weeks ago. On Wednesday, it was almost back to pre-banking crisis levels.

As bond yields have resumed a slow climb this week, the number of stocks advancing versus declining has improved daily. Beaten-up sectors like REITs, industrials, and materials, all deeply in the red this month, have begun to turn around this week.

It is good news the banking panic is calming down, but it means we will all go back to focusing on inflation, starting with Friday’s PCE. Fed Chair Jerome Powell, when he met with Republican Congressional leaders this week, reminded them that the current forecast calls for at least one more additional rate hike of a quarter percentage point.

Markets are pricing the best of both worlds: a recession that brings inflation down rapidly and keeps rates low, yet one where corporate earnings do not fall sharply. Still, we should be sceptical and think bonds and stocks look expensive.”

Indeed, the S&P is currently trading for roughly 18 times 2023 earnings estimates. That would be a pricey multiple, even in an economic expansion. In an economic contraction, it constitutes a bit of magical thinking.

Alibaba’s outlook brightens after the split.

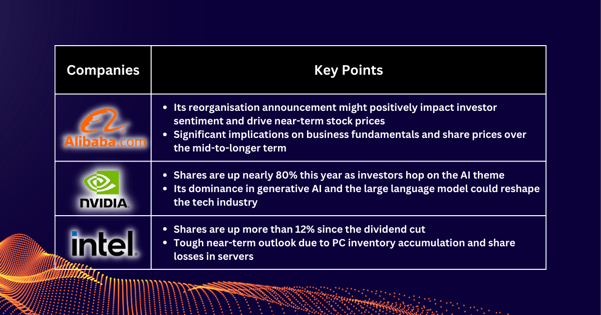

It is time to watch Alibaba shares as the outlook brightens following the company split. Alibaba shares have even further upside over the medium- and long-term, even after the e-commerce giant’s reorganisation announcement spurred the stock rallying.

From an investor sentiment impact perspective, they like Alibaba’s reorganisation to Google’s transformation to Alphabet, a clear sentiment booster that should drive near-term stock price.

Alibaba’s reorganisation could bring more significant implications to business fundamentals and share price over the mid-to-longer term. We expect a positive share price reaction to the reorganisation announcement.

Alibaba said on Tuesday that it would split its company into six business groups, a significant restructuring of the Chinese tech giant, except Taobao, which will remain wholly owned by Alibaba. Each company will have its CEO and board of directors, raise funding externally and go public.

Nvidia: Party has not been over.

Shares of Nvidia are up nearly 80% this year as investors hop into the AI theme. The company recently unveiled new products at partnerships at its developer conference and launched its DGX Cloud, which can be used to train models behind generative AI applications.

Wall Street analysts hailed Nvidia’s dominant leadership in AI after its conference. Nvidia’s dominance in generative AI and the large language model could reshape the tech industry.

Intel: Tough near-term outlook

Last month, Intel cut its dividend by nearly two-thirds to 12.5 cents per share, with the semiconductor maker also announcing a host of cost-cutting measures. Intel shares are up more than 12% since the dividend cut, outperforming the Dow.

However, inventory accumulation in PCs makes the near-term outlook for Client Computing harder than expected, with continued share losses in servers dragging further on revenue recovery.

Fullerton Markets Research Team

Your Committed Trading Partner