Policy divergence will continue to support the dollar, sell EUR/USD?

Fed is likely to continue the hiking pace even as stocks are selling off

US workers enjoyed the biggest leap in pay since 2009 as job gains topped forecasts and the unemployment rate held at a 48-year low, a boost for President Donald Trump ahead of this week’s midterm elections and reason for the Federal Reserve to keep raising interest rates.

Nonfarm payrolls rose 250,000 after a downwardly revised 118,000 gain, Labour Department report showed Friday. Average hourly earnings for private workers advanced 3.1% from a year earlier and the unemployment rate was unchanged from September at 3.7%, both matching projections.

The figures give Republicans another economic accomplishment to tout ahead of Tuesday’s midterm elections as they seek to defend control of Congress from what polls indicate will be Democratic gains. The continued hiring and wage increase also reflect a tax-cut boost and reinforce expectations that the Fed will raise interest rates for a fourth time this year in December, though such an outlook may further unsettle investors who just sent US stocks to their worst month since 2011.

Since the start of this year, the yield on the benchmark 10-year US Treasury bond has risen by 80 basis points to 3.21%, while the yield on the German 10-year bond has remained essentially unchanged at just over 0.4%. US Treasuries were well offered throughout the US session, extending overnight losses following a solid jobs report and positive turn in the trade deal talks with China. Trump told reporters he thinks the US will reach a trade deal with China. The current differential of almost 280 basis points is a huge historical outlier. Dispersion has also been the name of the game for two-year bonds, where the yield differential currently stands at over 350 basis points as the German notes persist in negative yield territory. At the same time, the dollar has strengthened by almost 5%, as measured by the DXY index.

But the policy gap with the Fed will not narrow much given the US central bank's determination to maintain a relatively aggressive rate of rate hikes as its balance sheet gradually shrinks. Meanwhile, the People's Bank of China seems conflicted about its exchange rate policy. It may not yet be the best time for investors to position themselves aggressively for convergence. And when the time comes for convergence, probably in the first half of 2019, there will be a lot of ways to translate this trade in investment portfolios, but it is too early at this moment.

Our Picks

EUR/USD – Slightly bearish.

USD strength this morning on the back of higher US Treasury yields post firm nonfarm payrolls data on Friday. Pair may drop towards 1.1335 this week.

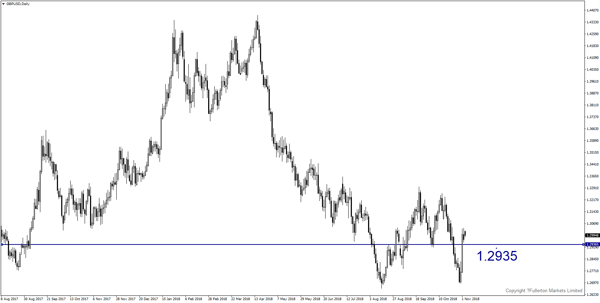

GBP/USD – Slightly bearish.

Investors that were stopped out of GBP/USD early on Monday have re-entered short positions amid speculation of early reports of a Brexit customs deal to be denied. This pair may drop towards 1.2935 this week.

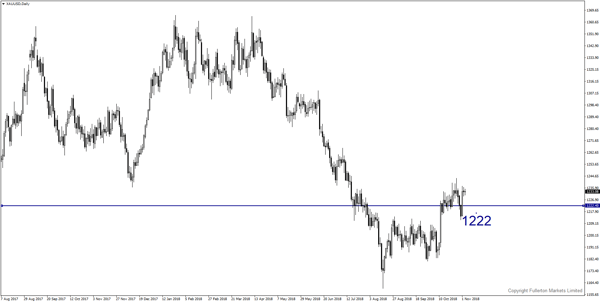

XAU/USD (Gold) – Slightly bearish.

We expect price to fall towards 1222 this week.

Fullerton Markets Research Team

Your Committed Trading Partner